Weekly Perspective: Learning to Live With It

There are 3 points to make in today’s note.

Jobs data was strong in July, showing continued healing in the U.S. labor market. Strong jobs data pushes the Fed to make a call on tapering, but it will likely try to hold off until the Fall when the backdrop is more “normal” (children return to school and supplemental benefits roll off). The surge in Delta cases is not having a meaningful impact on consumer behavior yet.

Jobs Data

Countering the downside surprise from Wednesday’s ADP private payrolls report, Friday’s July Nonfarm Payrolls came in above expectations at 943k jobs added, the largest gain in eleven months.

This 943k was above expectations of 870k, with the upside coming mostly from state and local hiring. Leisure and hospitality added 380k jobs in July, indicating continued improvement in the hard-hit services sector of the economy.

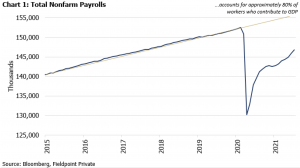

This brings the total number of people employed to 5.7 million below the pre-COVID peak. Recall that 22.1 million jobs were lost between January 2020 and April 2020. There have also been an estimated 1.2 million people who have chosen to retire since the COVID recession, and though these people might be coaxed back into the labor force by higher wages, this cohort is less likely to rejoin. This is one reason why it may take some time to return to the pre-COVID trend of employment shown in Chart 1.

The unemployment rate fell to 5.4% from 5.9% in July, with the total number of people gaining employment outweighing the 261k new entrants into the labor force. The WSJ article linked above estimates that 67% of the new hires last month were from workers that had previously not been in the labor force.

This displays that higher wages, falling supplemental unemployment benefits, and COVID fears fading are working to draw people back to work. There is an expectation that continued increases in vaccination rates, the return to in-person school (for those who don’t have access to child care), the complete roll-off of supplemental unemployment benefits in September, and a continued tight labor market putting upward pressure on wages will all serve to draw more people back into the labor force.

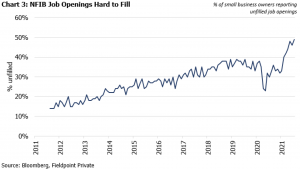

On the tightness of the labor force, job openings have reached a record 9.2 million open jobs in the U.S (Chart 2). Businesses continue to have trouble filling open positions, with the NFIB percentage of small businesses with job openings that are hard to fill at a record 49% (Chart 3).

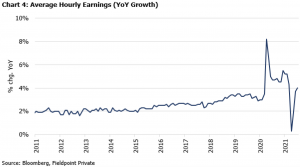

This tight labor market is putting bargaining power in the hands of workers and leading to a rebound in average hourly earnings growth as seen in Chart 4. Note there are distortions in this data from COVID because many of the job losses in 2020 were in lower wage sectors that boosted the average hourly earnings. Now we are seeing wage growth in the lower wage sectors that is helping to boost the index.

The conclusion is that the job market is now tight and wages are going up. The question will be how many workers will reenter the labor force as we enter in a more “normal” environment. From there, how will the Fed respond and how big of a threat is the Delta variant of COVID-19?

Fed Reaction

The more hawkish Fed governors, such as Governor Waller, think that strong jobs reports like we got on Friday, plus continued evidence of recovery, support kicking off tapering by October. Waller thinks that monthly jobs gains of 800k-1m over the next couple of months support tapering “early and fast” and opening a discussion of rate increases by mid-2022.

The Fed Chair and other more dovish members in the majority likely will want to wait until that more “normal” post-September environment to set a time for the taper, which likely means later in 2021 or at the start of 2022.

But even leading dove, Vice-Chair Clarida, said that the economy, in both employment and inflation, would support rate increases by the end of 2022 (meaning tapering would be completed before that). However, he noted the risk was to the upside for his inflation forecast, meaning “lift off” could come even sooner.

We note that inflation seems to be a rising “hot button” issue for voters and for politicians looking to push back on further fiscal stimulus. This likely increases political pressure on the Fed to move to incrementally tighten policy, and thus move away from its desire to be tolerant of and not act preemptively against inflation. This movement away from inflation tolerance could be one reason why long rates have been declining and the future expected “terminal” policy rate has been falling.

The conclusion here is that tapering is nearly certain for 2022, with possibility that it can come even sooner.

The pace of the recovery and economic growth is likely to slow from here, so the key risk for markets will be how set the Fed is on removing accommodation into a slowing growth momentum economy.

This is what happened in 2018. The Fed was on “autopilot” but growth was slowing rapidly. This led to a flatter yield curve, compressing equity multiples, sharp underperformance of cyclical assets, and of course, the December 2018 market melt-down.

Powell certainly would like to avoid that scenario again.

Delta Variant

The Delta variant of COVID-19 remains a real health risk and could be a source of surprise market volatility and weakness, but early data points to consumer behavior that is proving to be much more resilient to COVID risks than prior waves of infections. This means that outside of returning to lockdowns (like in Australia), the economy should be more resilient to the Delta wave than prior waves.

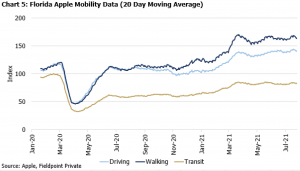

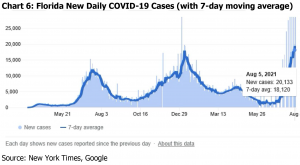

An example to support this is Florida’s mobility and COVID case data. Florida, my home state and the source of 1/3 of new COVID cases in the latest wave, has seen resilient mobility data despite the surge in cases (Chart 5 and Chart 6). This may exacerbate the case count in the short term as people keep normal behaviors, but indicates that people are learning to live with COVID.

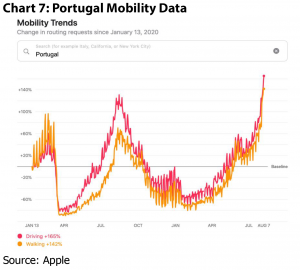

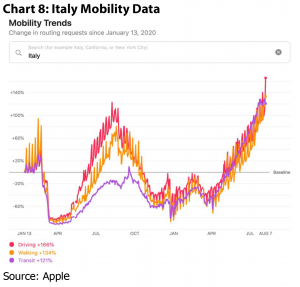

It is not just in the U.S., we can see huge surges in mobility data in popular holiday destinations in Europe, such as Italy and Portugal (Chart 7 and 8), despite new restrictions (such as vaccine requirements) and rising case counts. Nothing stands in the way of summer vacation.

As many epidemiologists predict, COVID-19 is likely here to stay, meaning we will continue to have to learn how to live with it. This could mean future booster shots and continued alterations to behavior (masking, distancing, etc.), but a return to lockdowns and their concomitant economic disruptions looks less likely based on the reaction to the most recent COVID wave.

Disclosures

IMPORTANT LEGAL INFORMATION

This material is for informational purposes only and is not intended to be an offer or solicitation to purchase or sell any security or to employ a specific investment strategy. It is intended solely for the information of those to whom it is distributed by Fieldpoint Private. No part of this material may be reproduced or retransmitted in any manner without prior written permission of Fieldpoint Private. Fieldpoint Private does not represent, warrant or guarantee that this material is accurate, complete or suitable for any purpose and it should not be used as the sole basis for investment decisions. The information used in preparing these materials may have been obtained from public sources. Fieldpoint Private assumes no responsibility for independent verification of such information and has relied on such information being complete and accurate in all material respects. Fieldpoint Private assumes no obligation to update or otherwise revise these materials. This material does not contain all of the information that a prospective investor may wish to consider and is not to be relied upon or used in substitution for the exercise of independent judgment. To the extent such information includes estimates and forecasts of future financial performance it may have been obtained from public or third-party sources. We have assumed that such estimates and forecasts have been reasonably prepared on bases reflecting the best currently available estimates and judgments of such sources or represent reasonable estimates. Any pricing or valuation of securities or other assets contained in this material is as of the date provided, as prices fluctuate on a daily basis. Past performance is not a guarantee of future results. Fieldpoint Private does not provide legal or tax advice. Nothing contained herein should be construed as tax, accounting or legal advice. Prior to investing you should consult your accounting, tax, and legal advisors to understand the implications of such an investment.

Fieldpoint Private Securities, LLC is a wholly-owned subsidiary of Fieldpoint Private Bank & Trust (the “Bank”). Wealth management, securities brokerage and investment advisory services offered by Fieldpoint Private Securities, LLC and/or any non-deposit investment products that ultimately may be acquired as a result of the Bank’s investment advisory services:

Such services are not deposits or other obligations of the Bank:

− Are not insured or guaranteed by the FDIC, any agency of the US or the Bank

− Are not a condition to the provision or term of any banking service or activity

− May be purchased from any agent or company and the member’s choice will not affect current or future credit decisions, and

− Involve investment risk, including possible loss of principal or loss of value.

© 2021 Fieldpoint Private

Banking Services: Fieldpoint Private Bank & Trust. Member FDIC.

Registered Investment Advisor: Fieldpoint Private Securities, LLC is an SEC Registered Investment Advisor and Broker Dealer. Member FINRA, MSRB and SIPC.