Johnny Gibson, CFA®, Chief Investment Officer

Cameron Dawson, CFA®, Chief Market Strategist

See below for your Weekly Perspectives from the Fieldpoint CIO Office. Here are the contents so you can focus on what is most relevant to you:

Weekly Perspective: Close Encounters of the 3P Kind

Well I guess you’ve noticed… something is a little strange with the bond market…

There is an iconic scene in Close Encounters of the Third Kind where Roy Neary (Richard Dreyfuss) becomes completely engrossed in building a tower out of mashed potatoes while at the dinner table. His family sits there, staring at his bizarre behavior, both confused and concerned.

We have all been the Neary family over the past couple of weeks, confused and concerned as we watch the bond market’s seemingly bizarre behavior.

Confused because bond yields are declining (bond prices are rising) despite apparently strong economic data and resilient risk asset prices.

Concerned because of what falling bond yields could be saying about the future path of economic growth, as well as market participants’ desire for defensive assets.

A clarifying note: in recent years, we often see U.S. bond yields rise when economic growth and inflation are strong/accelerating and fall when growth and inflation are weak/slowing. This is because of how growth and inflation are reflected in the components of bond yields, as well as investor appetite for risk, with defensive assets like bonds in greater demand when growth is faltering. This is why equites have often underperformed during periods of sharp bond yield declines (despite the benefit of the falling risk-free rate). This doesn’t always hold, but is a fine heuristic for this discussion at this time.

To try and make sense of this, we need to look at why bond yields are falling, and that’s where the 3P’s come in: Positioning, Peak Data, and Preemptive Fed (not Potatoes). Many prognosticators think the bond market is reacting to just the technical/positioning driver, but we think it is a mixture of all three.

Positioning

Positioning became very one-sided and even extreme through the spring (short Treasuries, short dollar, long commodities, and long Value/cyclical/reflation equities). This positioning has been enduring a pain trade in the opposite direction, reaching a fever-pitch of short covering and outflows last week.

There have also been supply and demand factors for Treasuries, where new Treasury supply has been low and demand has remained high (from the Fed’s QE, U.S. banks, and foreign investors), putting downward pressure on yields/upward pressure on prices.

Peak Data

Peak data and outright growth fears have been weighing on bond prices by pulling down out-year growth and inflation expectations. Even though absolute economic activity has remained strong, the pace of the expansion, along with the pace of policy support growth, is clearly slowing.

We also note that many positioning flows hit extremes just as peak data momentum was being achieved. Ain’t that a kick in the head.

Interestingly, we have not seen a distinct and sustained flight to quality and defensives in other areas of the market. Equites are still at all-time highs and credit spreads are still near all-time lows, signaling strong risk appetite. This is why the rally in bond prices is so divergent from the rest of the market. Either bonds are “right” and we are going into a growth challenged or deflationary period, or equites/risk-assets are “right” and growth will remain robust (which would make the recent move in bond yields more about the positioning/technical factors described above). We’ve written about this divergence a great deal in recent months (here, here, here, here).

Preemptive Fed

Lastly, the preemptive Fed could be making a comeback. Last summer the Fed said it would change. The Fed said it would now be tolerant and not preemptive when it came to inflation. No longer would it raise rates in anticipation of higher inflation, instead it would allow inflation to run above its 2% target for “some time”, making up for all of that time below target.

This was one of the catalysts of the tripling in bond yields that occurred over the following nine months, reaching a peak in March of 2021. Bond yields typically move higher with inflation, and if inflation was going to be tolerated, then yields needing to be much higher than the generational lows that were reached last summer.

Despite this messaging and the dovish tone to the June Fed meeting minutes, asserting that elevated inflation remains transitory and the economy is still far off from making “substantial further progress”, the post-meeting commentary from Fed members has been more hawkish. Numerous Fed members expressed distinct concern about inflation running too hot and arguing that a tapering of the bond buying program should commence in short order. These Fed members appear to be getting cold feet about tolerating higher inflation and seem to be returning to their old, preemptive ways.

The move lower in bond yields could reflect this marginally hawkish shift. If the Fed is going to be less tolerant of inflation, then it could move to “normalize” policy sooner (tapering followed by rate hikes), which means lower out-year growth and inflation expectations since the Fed would not be letting the economy “run hot”.

So where do we go from here?

We think identifying the 3P’s is also helpful in seeing how these drivers could impact bond yields from here.

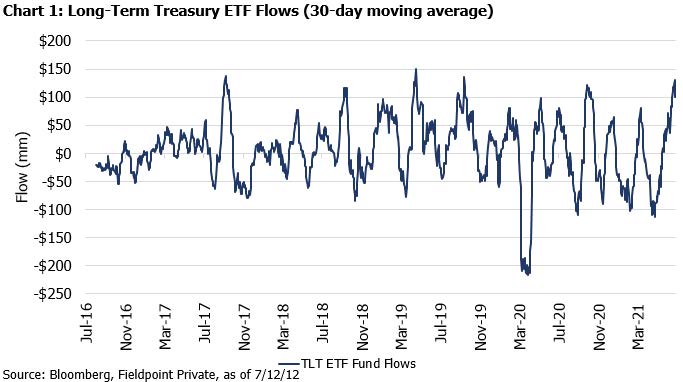

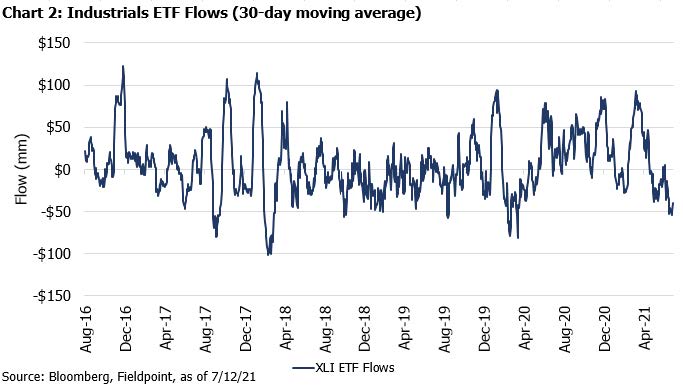

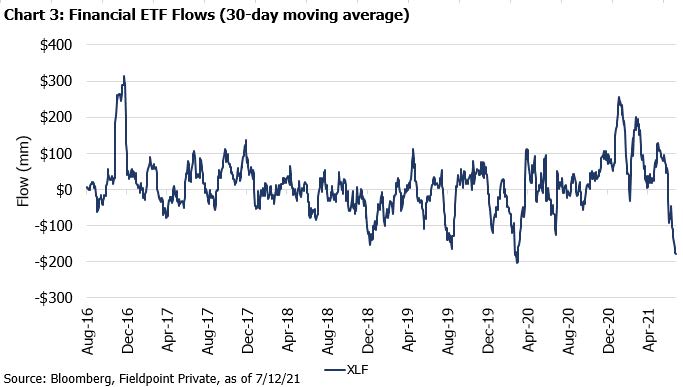

On positioning, we see evidence of a very quick, large reaction to last week’s moves, with huge inflows into long Treasury instruments and huge outflows from cyclical/Value parts of the equity market. These flows have reached extreme levels not seen since the initial COVID meltdown, which supports the notion that these trades (lower yields, lower cyclicals/value) could stabilize and possibly bounce (yields higher, value higher). See Chart 1 for flows into the long-term Treasury ETF and Chart 2 and 3 for flows out of cyclical ETFs for the industrial and financials sector.

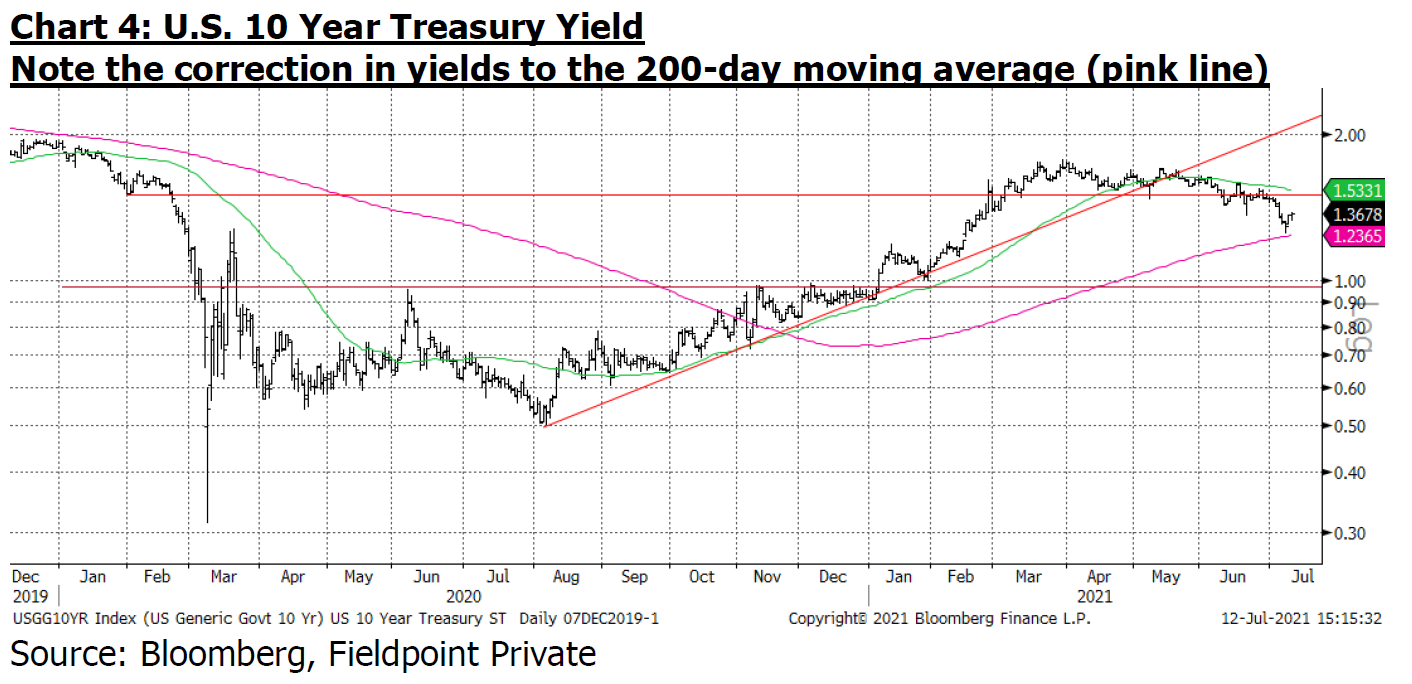

The 10 Year yield also traded to important support, right above its own upward sloping 200-day moving average (see Chart 4). This supports stabilization as well.

On peak data, we continue to see a moderation in data in the U.S. and globally. Whether it is PMIs, car prices, home sales, inflation, commodity prices, exports growth, or others, data is likely to continue to moderate from, along with the growth rate of both fiscal and monetary support. 2Q21 GDP and corporate earnings likely are the peak YoY growth rate we will see given the easy comparisons. This can continue to put downward pressure on yields, but the degree will depend on how much data surprises to the downside or has to be revised lower.

On the preemptive Fed, it likely won’t be until Jackson Hole that the Fed has a clear opportunity to strike a decidedly dovish tone. If it does not back away from the hawkish tilt, then expect further downward pressure on yields and the yield curve, as the market will continue to price in an earlier removal of extraordinary policy support.

We think the conclusion of these three factors for long bond yields is: a stabilization/stalling in the decline in yields, with potential for a bounce higher, though no clear catalyst for a significant and sustained move back to the March highs (for now). A break below the 200-day moving average would likely e a decided negative for risk assets, as it would indicate that we risk entering a deflationary shock.

Overall, it would behoove us to not completely write off the moves in the bond market as purely positioning or technical. We ignore the signal that the bond market is sending at our own peril, but we also need to be aware of those factors that drive short-term inefficiencies in the market (like short-covering rallies). Maybe we should just encapsulate this in the words of Roy Neary talking about his mashed potatoes again:

“This means something. This is important.”