Johnny Gibson, CFA®, Chief Investment Officer

Cameron Dawson, CFA®, Chief Market Strategist

See below for your Weekly Perspectives from the Fieldpoint CIO Office. Here are the contents so you can focus on what is most relevant to you:

Weekly Perspective: Hello Darkness, My Old Friend

(As we are writing this Monday morning, global equities markets are in the midst of a sell-off, while bonds are continuing to rally (yields lower). Prior to this downdraft, we had been in an incredibly resilient period for equities. In fact, it was the second longest period on record without a 5% correction (the longest was 2017). It had been a long time since we had talked to the darkness.

We have been identifying how both technical and fundamental risks were building in the market for some time (here, here, here, here, here), and so now these factors seem to be coming to a head. We have also publicly discussed the prospects for a 10-15% correction (see CNBC interview here) and also released a companion video that walks through the details of this expectation with a collection of charts (see video and chart deck here).

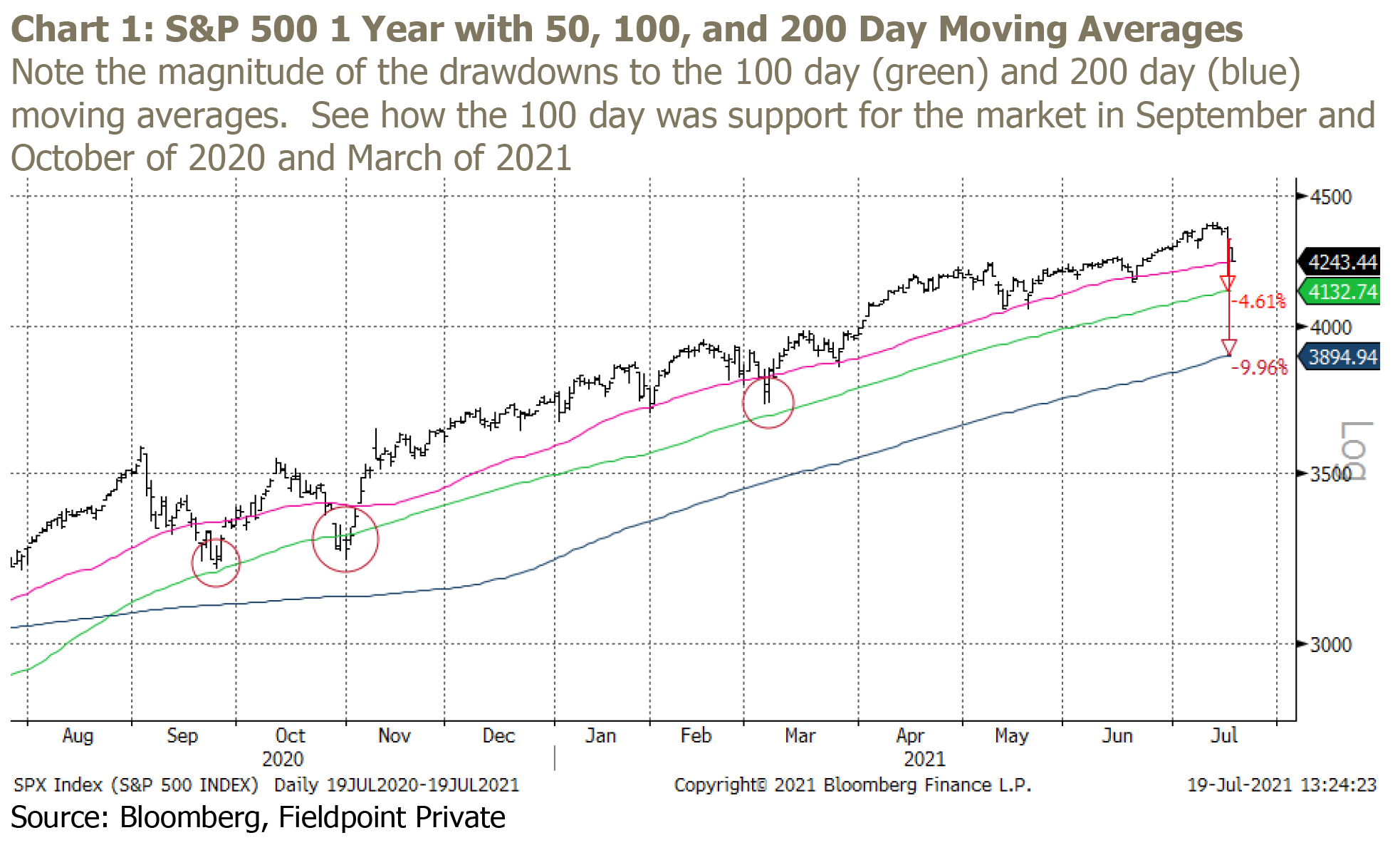

Our base case remains that we expect a moderate correction in the 10-15% magnitude (from Friday’s close, 10% brings you down to the 200 day moving average, 15% would be a slight overshoot). The bull case is a correction of only ~5% to the 100 day moving average, which has been the constant support level for equities in the Sep-20, Oct-20, and Mar-21 corrections. Chart 1 shows these levels.

This moderate base case correction is from our assessment that this would be a “technical positioning” correction (driven by both technical and fundamental factors) and not a response to significant deterioration in underlying fundamentals towards a recession, which would be the bear case.

Holding off this bear case for now is that we do not see signs that point to an imminent recession (such as credit spreads widening significantly, the 10-2 curve inverting, or consumer credit deteriorating).

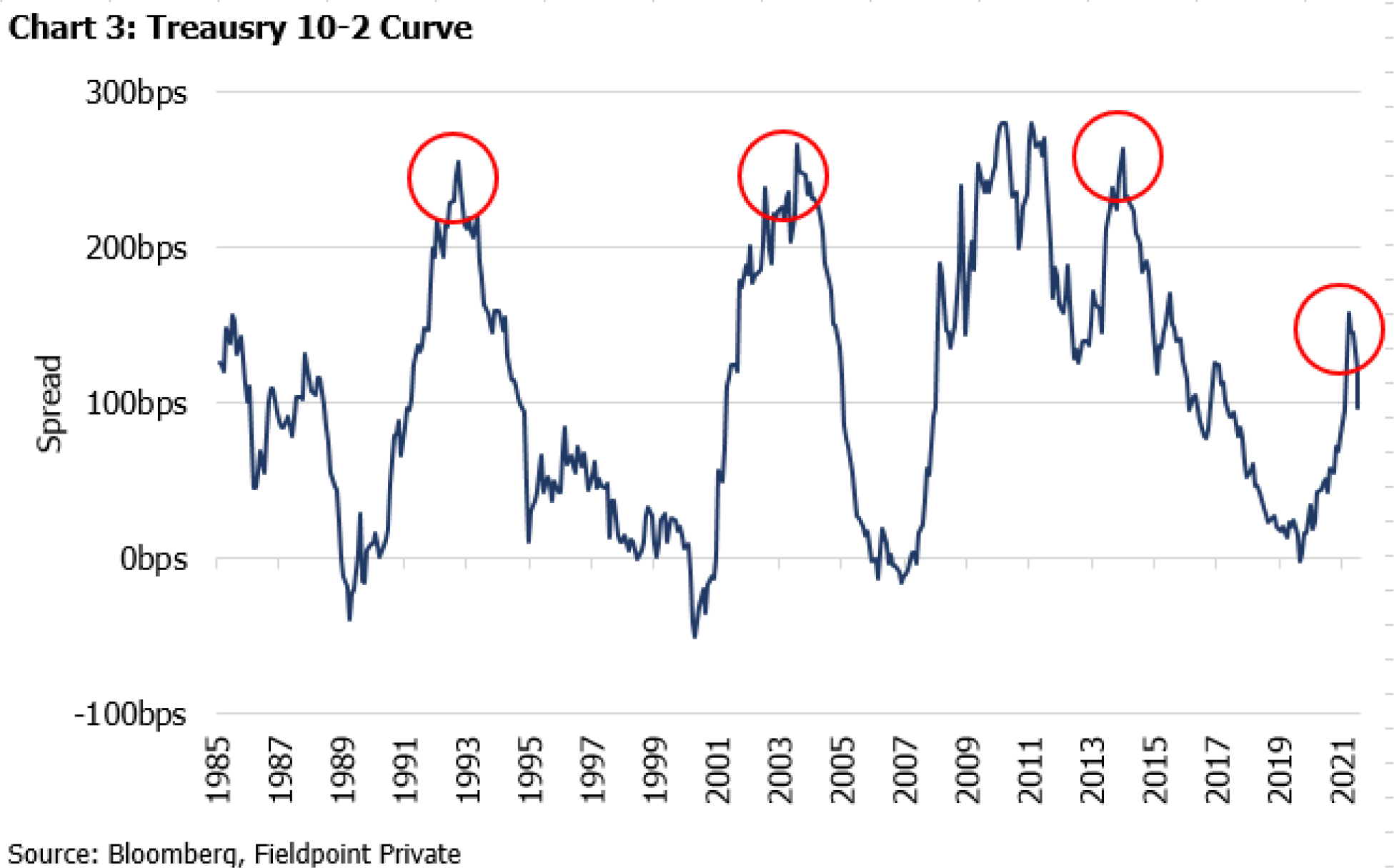

Of course we could see a larger correction without a recession indication if the market perceives that the Fed is making a policy mistake by tightening too soon, similar to 2018 (recall the 10-2 curve didn’t invert until 2019 but the correction was caused by fears that a recession would be all but certain if the Fed continued to tighten policy, even as unemployment remained near a 50 year low). We discuss the curve in detail below, but at a mere 98 bps as of today, a further flattening of the curve would be a negative for equity markets as it would signal a greater slowing in growth with policy moving too tight.

Back to the base case, we do see plenty of signs that equity markets were and are vulnerable to a moderate correction in the near term. We detail these in the video above and the attached asset allocation bulletin, but they include: fading breadth, fading momentum, being at the high end of long term trading ranges, stretched positioning, stretched valuations, peak data, peak policy support/liquidity, rising growth fears leading to a recalibration of expectations, and more.

We have been describing this environment as one with record inflows + near-record valuations + markets at all-time highs + high earnings expectations. This equals an environment where it is very difficult to surprise to the upside, and so either a negative catalyst or even a lack of a positive catalyst could drive a notable downside move as positioning, expectations, and valuations are recalibrated.

This kind of correction would be a healthy opportunity for the market to reset and prevent the building of excesses. The lead up to this correction has also been an opportunity for investors to be patient putting capital to work in equities in order to buy at a more attractive valuation.

For long-term investors with high tax sensitivity and trading frictions, the short duration and moderate magnitude of this expected correction likely warrants “riding out” the correction and focusing on using the volatility opportunistically to deploy capital into equities where possible/needed. With low tax sensitivity and greater flexibility, a short term defensive posture is warranted (lower equities, more defensive equites, higher cash), with the important note that a reversal of this positioning to being more risk-on could need to be executed in fairly short order. Markets sure do move fast these days.

And the Sign Flashed Out Its Warning:

Further Thoughts on Yields and the Curve

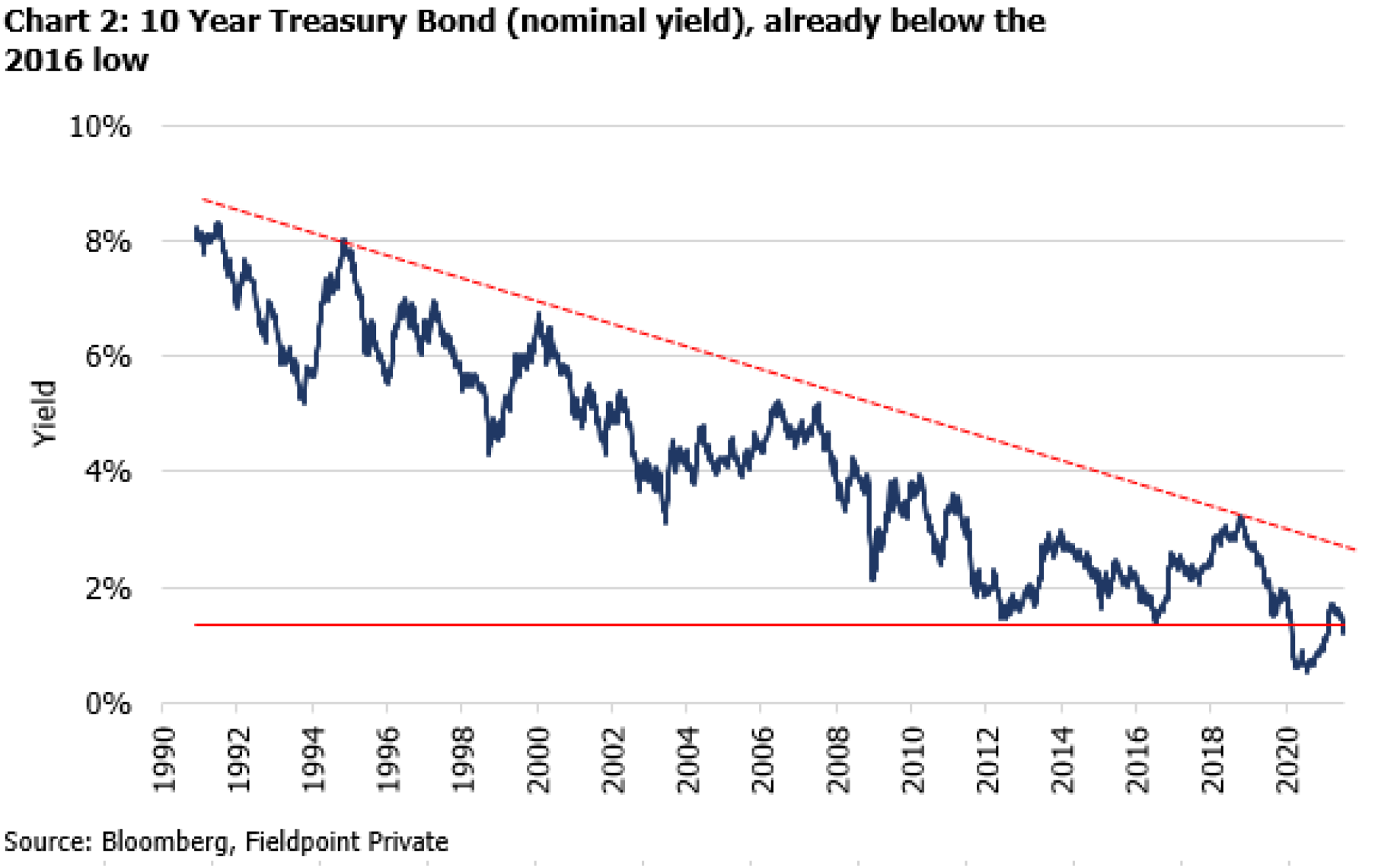

It is also incredible to note that the 10-2 curve (the difference in yield between the 10 year Treasury and the 2 year Treasury) is now below 100 bps (Chart 3). It is distinctly possible that we have already seen the peak in the yield curve for this recovery/cycle at a mere 150 bps. And the Fed hasn’t even done anything! Just a slight move to hawkishness by a few traditionally hawkish Fed members and an acknowledgment that they were “talking about talking about tapering”.

This low level of the yield curve leaves the Fed with very little wiggle room to negotiate a “normalization” and tightening of policy, as the market is proving to be hyper-sensitive to even the discussion of policy removal.

In 2018/2019 the curve was flattening and eventually inverted, resulting in the Fed being forced to abandon its planned rate hike and balance sheet run-off. The Fed eventually moved to cut interest rates in 2019 despite still having a 50-year low unemployment rate.

We find ourselves having to continuously lower our expectations of “normal”. The terminal policy rate that can be achieved this cycle is likely much lower than prior cycles (meaning the Fed won’t be able to raise rates much).

There is also a possibility that the QE bond buying becomes perpetual and is not tapered, mostly for the $80B of Treasuries a month. This is increasingly possible given high debt balances necessitate low interest rates in order to keep the interest rate on debt less than the growth rate of the economy. This is essentially curve control and follows the policy strategy of the Bank of Japan, which now owns (read “has retired”) over 50% of outstanding government bonds. This is also a policy tool suggested by Modern Monetary Theory to facilitate greater deficit spending to help the economy reach its full potential.

Now of course there are other factors leading to this bond rally (yields falling) that are beyond the forward expectations for fed policy, inflation, and growth. Positioning and flows are important too. As investors rush to unwind short bond positions (bets on yields moving higher) and deal with limited new Treasury supply, there is a point that yields will get oversold (bonds overbought) and a stabilization can occur. We noted last week that flows into long-dated Treasury bonds had reached an extreme (a sign of bonds being overbought). This could cause a stabilization in the fall in rates and in the flattening of the yield curve.

However, to see a full re-steepening move of the yield curve to new highs, we think policy and commentary about policy would have to turn even more accommodative than it is now. This is a repeat of 2012, 2016, 2019 where the Fed had to reverse course on less-accommodation/tightening plans in order to stabilize hyper-sensitive markets. The difference today is that markets are still enjoying the benefits of ultra-accommodative policy and yet are already pitching a fit. COVID disruption and its $5 Trillion of U.S. fiscal stimulus has not been enough to change the long term trends (debt, demographics, technology, etc.) that have been pushing yields down and necessitating greater and greater policy intervention.

Maybe very dovish commentary at the Fed’s July policy meeting or its August Jackson Hole meeting will be enough to assure markets and spark a re-steepening through the end of the year (helped by positioning becoming too long Treasuries by that point). But if they continue to argue for near term tapering and keep a focus on inflation fears, then this curve flattening has the potential to continue.

For the sake of extending the duration of this cycle, let’s hope the doves disturb the sound of silence…

IMPORTANT LEGAL INFORMATION

This material is for informational purposes only and is not intended to be an offer or solicitation to purchase or sell any security or to employ a specific investment strategy. It is intended solely for the information of those to whom it is distributed by Fieldpoint Private. No part of this material may be reproduced or retransmitted in any manner without prior written permission of Fieldpoint Private. Fieldpoint Private does not represent, warrant or guarantee that this material is accurate, complete or suitable for any purpose and it should not be used as the sole basis for investment decisions. The information used in preparing these materials may have been obtained from public sources. Fieldpoint Private assumes no responsibility for independent verification of such information and has relied on such information being complete and accurate in all material respects. Fieldpoint Private assumes no obligation to update or otherwise revise these materials. This material does not purport to contain all of the information that a prospective investor may wish to consider and is not to be relied upon or used in substitution for the exercise of independent judgment. To the extent such information includes estimates and forecasts of future financial performance it may have been obtained from public or third-party sources. We have assumed that such estimates and forecasts have been reasonably prepared on bases reflecting the best currently available estimates and judgments of such sources or represent reasonable estimates. Any pricing or valuation of securities or other assets contained in this material is as of date provided as prices fluctuate on a daily basis. Past performance is not a guarantee of future results. Fieldpoint Private does not provide legal or tax advice. Nothing contained herein should be construed as tax, accounting or legal advice. Prior to investing you should consult your accounting, tax, and legal advisors to understand the implications of such an investment. You may disclose to any and all persons, without limitation of any kind, the tax treatment and tax structure of any transactions contemplated by these materials and all materials of any kind, (including opinions or other tax analyses), that are provided to you relating to such tax treatment and structure. For this purpose, the tax treatment of any transaction is the purported or claimed U.S. federal income tax treatment of the transaction and the tax structure of a transaction is any fact that may be relevant to understanding the purported or claimed U.S. federal income tax treatment of the transaction.

Are not FDIC Insured – Are Not Bank Guaranteed – May Lose Value

Wealth management, securities brokerage and investment advisory services offered by Fieldpoint Private Bank & Trust (the “Bank”) and/or any non-deposit investment products which ultimately may be acquired as a result of the Bank’s investment advisory services: Are not deposits or other obligations of the Bank:

⦁ Are not insured or guaranteed by the FDIC, any agency of the U.S. or the Bank;

⦁ Are not a condition to the provision or term of any banking service or activity;

⦁ May be purchased from any agent or company and the member’s choice will not affect current or future credit decisions; and involve investment risk, including possible loss of principal or loss of value.

© 2021 Fieldpoint Private

Banking Services: Fieldpoint Private Bank & Trust

Registered Investment Advisors: Fieldpoint Private Securities, LLC, is a SEC Registered Investment Advisor and Broker Dealer. Member FINRA, SIPC.