Johnny Gibson, CFA®, Chief Investment Officer

Cameron Dawson, CFA®, Chief Market Strategist

See below for your Weekly Perspectives from the Fieldpoint CIO Office. Here are the contents so you can focus on what is most relevant to you:

Weekly Perspective: Summer Study Abroad

Promising the same depth of local immersion as a discount “12 countries in 20 days” backpacking tour of Europe (or an afternoon at EPCOT’s Food & Wine Festival for those who know), we are going to look at international markets today.

We are not going to go out of our depth to provide thorough country assessments, but instead look at what the broad make-up of the indices and their relative performance can tell us about the future prospects of these non-U.S. markets.

To give you the conclusion up front, the underperformance of developed and emerging markets versus the U.S. is showing no signs of abating yet. Both developed and emerging indices have made new relative lows vs. the U.S. in recent days, meaning the downtrends are firmly in place. Let’s dive into why and provide some thoughts about what could cause this underperformance to reverse.

Note: we use the S&P 500 Index for the U.S., MSCI EAFE Index for the developed market ex-US, and MSCI EM Index for emerging markets.

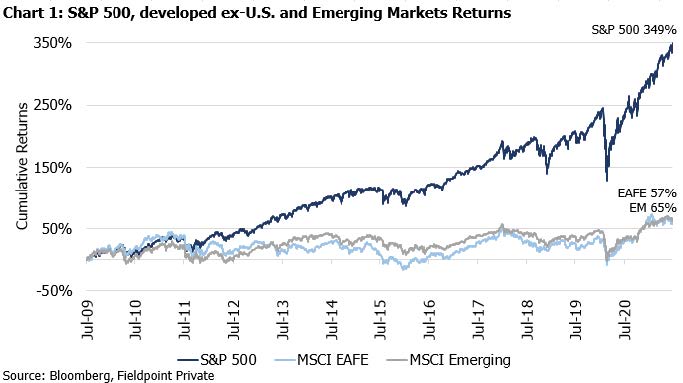

The starting point of this discussion is that international market indices, both developed and emerging, have underperformed the U.S. by a massive degree over the past decade. Coming out of the Great Financial Crisis (GFC) recession, since 2009 developed and emerging markets have underperformed the U.S. S&P 500 by nearly 300%. Chart 1 throws this underperformance into sharp, and harsh, relief:

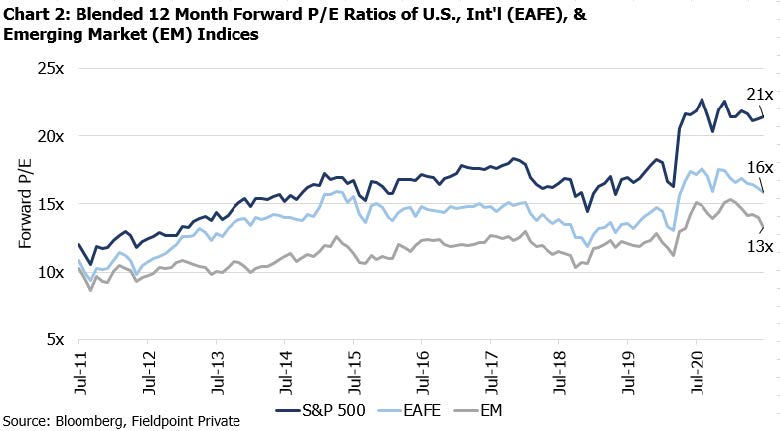

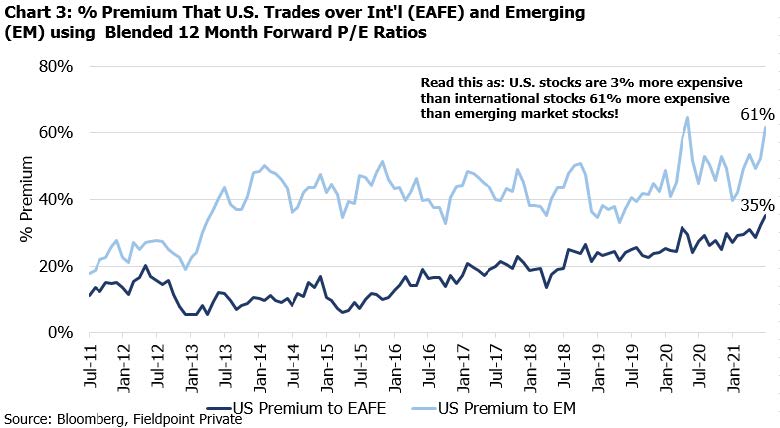

This degree of U.S. outperformance has also resulted in the U.S. trading at a significant premium in valuation to both developed and emerging markets. Chart 2 shows the forward PE ratio for each index, while Chart 3 plots the premium at which the U.S. is trading over the developed and emerging indices. These charts reveal far more multiple expansion in the U.S. over the past decade, resulting in U.S. markets trading at a 10-year high premium to developed and EM indices.

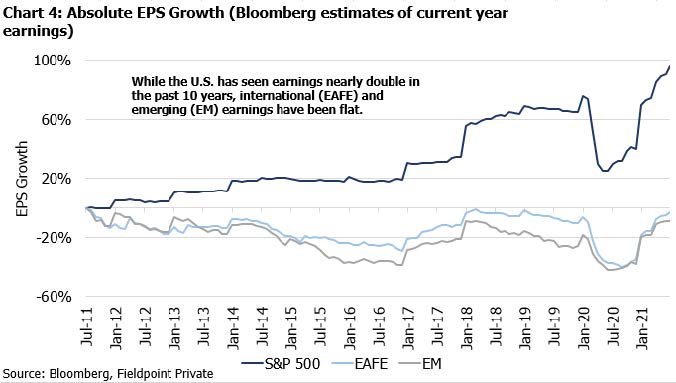

But it’s not just valuations that have driven U.S. outperformance, it’s also the growth of fundamental earnings that has set the U.S. apart. Using Bloomberg’s current year estimates for aggregate earnings of each index, we can see in Chart 4 that both developed and emerging indices have not grown the level of total earnings in the past 10 years! Compare that to the U.S.’s doubling of earnings in that time, and the rest of the picture of outperformance takes shape.

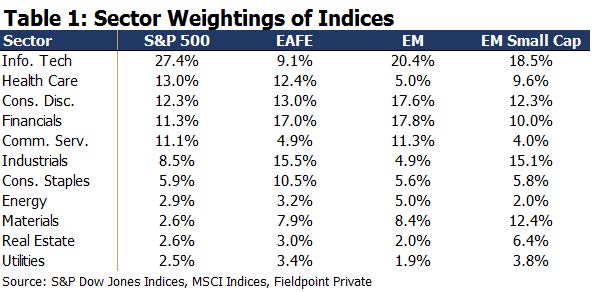

A common explanation of why the U.S. has enjoyed more multiple expansion and earnings growth than the rest of the world is the sector make up of its index (Table 1 provides a breakdown of each index by sector). The U.S. index has its largest weight in the Technology sector, which is associated with higher earnings growth as well as premium multiples (better margins, cash flow, consistency and growth potential are often cited as reasons for the Technology premium). Note, some dominant consumer discretionary and communication stocks are often included in the discussion of the “tech” cohort.

One reason for this ultra-dominant performance out of U.S. tech/consumer has been the contribution of the U.S. growth giants: FANG or FAANGM+ (and similar acronyms). An analysis done by Bernstein’s Quant Team and shared by Corey Wang shows that ex-FAAMG, the U.S. tech sector has grown earnings just in line with the broader market. We can see in analysis done by Yardeni Research, that the narrow FANG (FB, AMZN, NFLX, GOOGL both classes) has grown from 3% of the S&P 500 market cap in 2013 to 13% today, with earnings going from 1% of the S&P 500 to nearly 6% today. The nearly 1,200% return of FANG has contributed 30 percentage points of total performance to the S&P 500 since 2013. FANG has also contributed about 1.6 multiple turns to the S&P 500 valuation.

This tech dominance contrasts with the international developed market sector breakdown, where the index is dominated by Financials and Industrials. These sectors have continuously lagged given factors like regulation and macro headwinds. For example, international Financials have struggled in a world of flat yield curves that contain negative interest rates, with further challenges from weak balance sheets and heavy regulation following the GFC. Industrials have struggled in a world of weak commodity prices (these companies often serve commodity end markets) and tepid global growth and inflation since the GFC (their mature businesses are highly correlated to global nominal GDP growth).

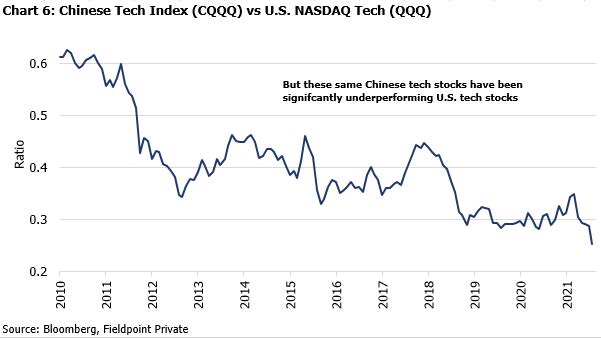

Interestingly, the emerging markets sector breakdown has a closer weighting to Technology compared to the U.S., but it is important to note that a lot of the tech weighting in the EM index comes from Chinese tech stocks. Chart 5 shows how Chinese tech stocks (CQQQ) have outperformed the China MSCI index, but then Chart 6 shows how these same Chinese tech stocks have significantly lagged U.S. tech/growth stocks (QQQ) for an extended period of time (long before this most recent crackdown on Chinese tech companies, which is causing significant underperformance in these shares).

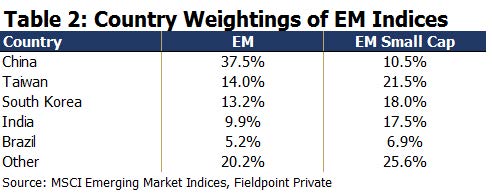

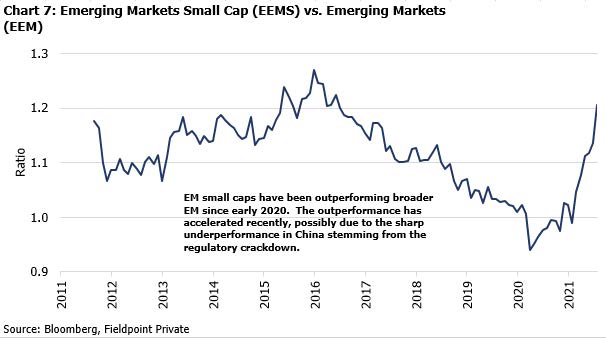

On a similar note, we find it interesting that EM small-cap has been outperforming sharply since early 2020, with huge outperformance in 2021 (see Chart 7). You could interpret this as a sign of rising risk appetite amongst EM investors (willingness to invest in smaller, nascent companies is often a sign of investors desire to take on risk). Another explanation is that this is a reflection that many of the most exciting “new economy” companies that have large growth potential are still small compared to the larger, often state-backed, mature companies. But we also think that the EM small-cap outperformance vs. EM is driven by the lower weighting to China in EM small-cap (see Table 2).

So all of this leads to the ultimate question: after nearly fifteen years of underperformance by international and emerging indices, what could possibly drive a reversal in this downtrend and end the era of U.S. market dominance?

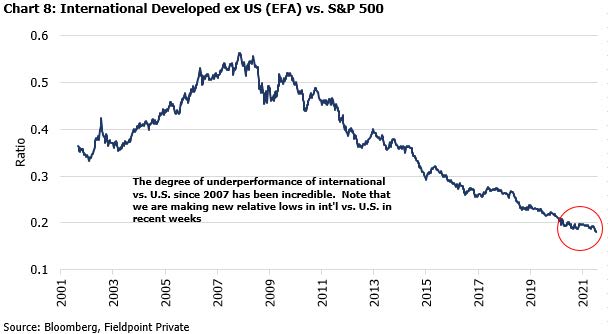

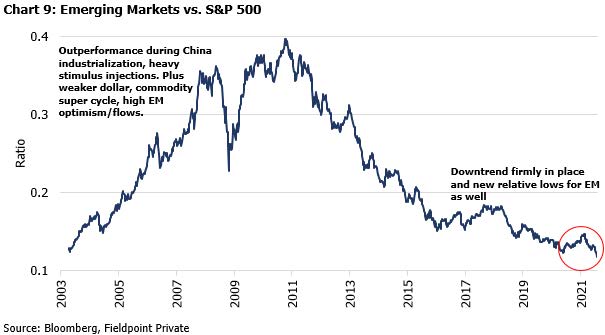

The first way to answer this question is to simply let the relative performance charts tell us when the underperformance is over. Both international and emerging market indices have been in a distinct relative downtrend vs. the U.S. for over a decade shown in Chart 8 and Chart 9. Both indices have recently made new relative lows in recent weeks, meaning that the degree of underperformance continues to widen. Until we see this downtrend in relative performance end, it is hard to call the end to U.S. market dominance.

We think these relative charts are fascinating because they exhibit that even though you could have made “rotation into international/EM” call driven by valuation or mean-reversion of performance at any point in the past decade, the underperformance has been relentless. We may be “late” by waiting for these relative charts to turn and end the downtrends, but waiting for confirmation can avoid buying into value traps.

Chart 8 and Chart 9 also raise an interesting question about what drove the last period of sustained international outperformance, which was in the 2000’s. We have already answered part of this question, which is the difference in sector weightings. Unlike today’s market of Growth/tech dominance, the 2000’s were led by Value shares, which had and have a much larger representation in international/EM indices.

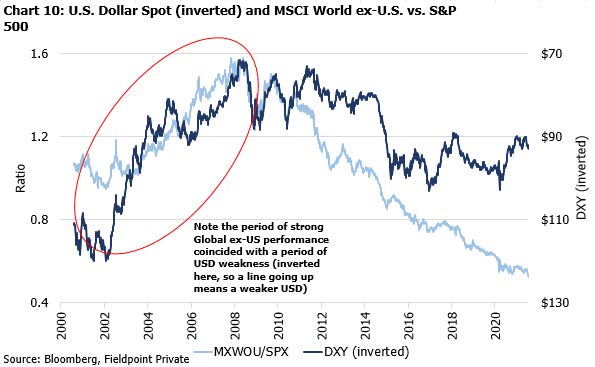

This 2000’ Value outperformance was driven by the unwind of the tech bubble, as well as major macro shifts like a distinct weakening in the dollar (Chart 10 shows the dollar weakening with the MSCI World Ex US index) and a huge rally in commodities. The commodity rally was driven in large part by the rapid industrialization and infrastructure build-out of China (as necessitated by demand generated from China’s ascension into the WTO in 2001). China’s huge spending and ravenous consumption of raw materials kept lifting emerging markets until 2011 when the commodity supercycle peaked and China started moderating its stimulus spending (recall they had stepped spending up even more to shelter their domestic economy from the GFC). The subsequent fall in commodity prices left highly indebted EM economies in trouble and pressured the commodity-sensitive sectors that had come to dominate this index (Table 3 shows the EM sector weightings over time and how they became dominated by Energy and Materials during the 2000’s but have since become more weighted to Growth/tech today).

It is important to note that optimism on emerging markets also ran high in the 2000’s, as is often the case when outperformance is sustained. With the coining of the BRIC acronym (Brazil, Russia, India, China), and the inclusion of EM as a high-return asset class in institutional asset allocations, investors were eager to get a piece of the untapped fortunes in far flung places (which often required extrapolating unsustainable profit growth and/or ignoring serious financial risks). The weakening of the USD kept adding fuel to this fire.

So back to the question of what is the path forward.

We think a weaker dollar remains critical for int’l/EM outperformance. Acknowledging the chicken and egg conundrum (which comes first), a prolonged weakening of the dollar is likely the key driver to see a sustained flow of capital out of the U.S. and into int’l/EM, which would help relative outperformance.

There have been fears expressed and arguments made that the U.S.’s experiment with large deficit spending monetized by the Fed in response to COVID would put downward pressure on the USD. It certainly hasn’t happened yet, but possibly because the future path of inflation remains highly uncertain. If inflation does prove to be transitory, then the fears of debasement of the USD fear are likely misplaced for now. Reflecting this fear, there was large short positioning built in the USD to start 2021, which has contributed to recent USD strength as the short positioning has been unwound. Another reason for USD resiliency could be that other countries are stimulating as well. If the U.S. moves to keep both fiscal and monetary policy easier than global peers (many of which are now starting to taper or raise rates), then maybe we could see a return to USD weakness. Clearly there are a lot of countervailing forces here.

Long term factors like demographics are also notable. Demographics do favor emerging markets, but we note that demographics have been favorable for emerging markets during this entire last decade of underperformance. Developed markets like Japan and Europe have a demographic headwind due to their aging populations.

There is also the potential for better non-U.S. performance driven by new tech companies that bring network businesses to less developed economies. This may not be enough to drive index level outperformance, but certainly is fertile ground for individual company investing, as we have seen a few notable success cases in recent years.

Overall, we come back to the conclusion with which we started. The trend of underperformance in international developed and emerging markets continues. After a decade of underperformance and with cheap valuations, the conditions are certainly enticing for better non-U.S. performance (in fact our asset allocation models have higher expected returns over the next decade for the int’l/EM asset classes). However, as the relative performance charts show, timing is important, and we still need a catalyst to drive this rotation and an end to the downtrend in relative performance. And so, we’ll keep looking for this catalyst like an American tourist abroad looking for wi-fi and hamburgers (I’ve been there!).