All That Glitters is Goldilocks? The Setup for 2022

Believe it or not, November 8, 2021, marks the 50th anniversary of Led Zeppelin IV (also known as “the fourth album,” Runes, Untitled, Four Symbols, and ZoSo).

The album was powered by the resentment that the band had for music critics, who claimed that Led Zeppelin’s success was “driven by hype and not talent,” according to bandmember Jimmy Page.

Critics continued to doubt the band upon the release of the album (radio stations even pressed for a shortened version of “Stairway to Heaven,” which we can agree would have been criminal).

But the critics were proven wildly wrong. Led Zeppelin IV went on to not only be the source of definitive hits for the band, but also to become one of the best-selling rock albums of all time.

In many ways today’s S&P 500 bull run is a lot like Led Zeppelin IV: doubted by critics but stacking up to be one of the greatest of all time.

Starting the year, there were plenty of things for market critics (ourselves included) to call out as potential stumbling blocks that could drive lower returns in 2021: high valuations, evidence of irrational exuberance and excessive risk taking, strong price appreciation in the prior two years (+29% in 2019, +16% in 2020), slowing growth of both fiscal and monetary support and risk of margin pressure from inflation, to name a few.

But at +25% YTD on the S&P 500, the critics have certainly been proven wrong this year.

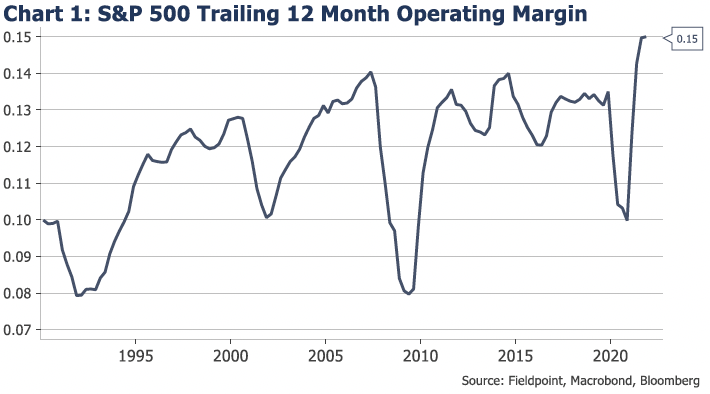

In many ways we have had an extended “Goldilocks” market: earnings growth has been extraordinarily high on the back of reopening dynamics, stimulus and tech strength, inflation has not been enough to upset earnings with S&P 500 operating margins at a record 15% (see Chart 1), and the Fed remaining very accommodative despite higher inflation, keeping liquidity abundant.

This latter point about ample liquidity is important because it has allowed S&P 500 valuations to remain fairly elevated at 22x, meaning P/E multiple compression has not completely offset the higher earnings growth (as it did in 2018).

This year’s stellar performance brings the S&P 500’s three-year price increase to 87%. There are only three other periods of similar returns: the late 1990’s tech bubble, the mid-1950’s post-WWII boom and the mid-1940’s post-depression and war time rebound.

So the question is: can this rally continue with similar gusto, or are we wise to recycle our list of headwinds from 2021 and expect lower returns in 2022?

We think it is the latter, with expectations that price appreciation should moderate next year. This does not mean to be uninvested, we just need to temper our upside expectations.

First, it would be exceptional to see the S&P continue to rally at such a breakneck pace. It is rare to see three years of consecutive S&P 500 returns over 15% as we have seen (it has only happened four times in the history of the index), but it is even more rare to see four years in a row of returns over 15%.

Looking at the entire history of the S&P 500, we found only one other period where there were four years of S&P 500 returns over 15%: the late 1990’s equity bubble.

To expect a repeat of that bubble performance, investors must also be aware of what came on the other side of that powerful performance: a painful, rolling 3-year bear market.

Similarly, following each of the periods we listed above where 3-year performance was elevated, the S&P 500 experienced a down year in the subsequent year (2000 -10%, 1957 -14%, 1946 -12%).

A down year is not our base case for 2022, but this historical experience of strong returns today sowing the seeds for lower returns tomorrow, does make us attune to the potential risks facing equites in 2022 (a stronger dollar, geopolitical risks, inflation, tighter monetary policy, to list a few).

To get to expectations for price growth in 2022, it is helpful to think about price returns in their two components: earnings growth and the price (or multiple) you pay for those earnings.

This year earnings have expanded mightily, with FactSet estimates for 47% earnings growth in 2021. This growth is expected to slow materially in 2022 to just 7%.

This number for 2022 earnings ($221.50) may be too low, as Street estimates have consistently needed to be ratcheted higher in the post-pandemic world (both revenues and margins have significantly surprised to the upside in the past 18 months).

So let’s assume some upside, with earnings growth shaking out to be about 10% in 2022. If you assume today’s P/E multiple of ~22x stays constant, you get a price return of 10% in the S&P 500.

But what if that multiple compresses? What could cause that multiple to compress?

This is where the Fed and its tightening plans become important watch items.

We expect P/E multiples to continue to compress as the Fed moves to taper QE and then eventually tighten monetary policy given the health of the underlying economy and job market, plus elevated inflation.

We also have to be aware that as inflation moderates (expected in 2Q22), this would effectively put upward pressure on real yields (nominal yields minus inflation), which would put downward pressure on tech/growth/FAANGM+ valuations. These stock valuations have been huge beneficiaries of deeply negative real interest rates, so if these real interest rates move higher as inflation moderates, this could be another source of multiple compression.

The reality that earnings growth will likely be slower next year means that there is less cushion for earnings growth to offset that multiple compression, as it has so effectively done this year.

When you add the two together, earnings growing more slowly and multiples compressing, you can see the fundamental underpinning for expecting lower returns in 2022.

The upside case here would be for earnings growth to surprise significantly to the upside, but we have to consider headwinds like the fiscal cliff, continued supply chain challenges, and simply tough growth comparisons.

The other upside driver would be for multiples to expand and not contract. What could cause that? One would be the Fed backing off of tightening liquidity and instead doubling down on accommodation (but here we think that the economic picture would have to get a lot worse in order to justify such a move, meaning markets would get worse before they got better). The other would be for multiples to expand and not contract, which would put us in bubble/melt-up territory, meaning risks would mount significantly for when the bubble pops on the other side.

Thus, we think the healthiest path forward for the market is more pedestrian returns for 2022, meaning 2022 may not be another Led Zeppelin IV collection of absolute bangers, but we would gladly accept Houses of the Holy and call it a day.

Disclosures

IMPORTANT LEGAL INFORMATION

This material is for informational purposes only and is not intended to be an offer or solicitation to purchase or sell any security or to employ a specific investment strategy. It is intended solely for the information of those to whom it is distributed by Fieldpoint Private. No part of this material may be reproduced or retransmitted in any manner without prior written permission of Fieldpoint Private. Fieldpoint Private does not represent, warrant or guarantee that this material is accurate, complete or suitable for any purpose and it should not be used as the sole basis for investment decisions. The information used in preparing these materials may have been obtained from public sources. Fieldpoint Private assumes no responsibility for independent verification of such information and has relied on such information being complete and accurate in all material respects. Fieldpoint Private assumes no obligation to update or otherwise revise these materials. This material does not contain all of the information that a prospective investor may wish to consider and is not to be relied upon or used in substitution for the exercise of independent judgment. To the extent such information includes estimates and forecasts of future financial performance it may have been obtained from public or third-party sources. We have assumed that such estimates and forecasts have been reasonably prepared on bases reflecting the best currently available estimates and judgments of such sources or represent reasonable estimates. Any pricing or valuation of securities or other assets contained in this material is as of the date provided, as prices fluctuate on a daily basis. Past performance is not a guarantee of future results. Fieldpoint Private does not provide legal or tax advice. Nothing contained herein should be construed as tax, accounting or legal advice. Prior to investing you should consult your accounting, tax, and legal advisors to understand the implications of such an investment.

Fieldpoint Private Securities, LLC is a wholly-owned subsidiary of Fieldpoint Private Bank & Trust (the “Bank”). Wealth management, securities brokerage and investment advisory services offered by Fieldpoint Private Securities, LLC and/or any non-deposit investment products that ultimately may be acquired as a result of the Bank’s investment advisory services:

Such services are not deposits or other obligations of the Bank:

− Are not insured or guaranteed by the FDIC, any agency of the US or the Bank

− Are not a condition to the provision or term of any banking service or activity

− May be purchased from any agent or company and the member’s choice will not affect current or future credit decisions, and

− Involve investment risk, including possible loss of principal or loss of value.

© 2021 Fieldpoint Private

Banking Services: Fieldpoint Private Bank & Trust. Member FDIC.

Registered Investment Advisor: Fieldpoint Private Securities, LLC is an SEC Registered Investment Advisor and Broker Dealer. Member FINRA, MSRB and SIPC.

Cameron Dawson

CFA®,

Chief Market

Strategist